Why Insurance Is Not Paying Your Water Damage Claim (And What It Means for You)

Why insurance not paying my water damage claim is one of the most common and frustrating situations a property owner can face after a disaster. Here are the most frequent reasons insurers deny or underpay water damage claims: (These are generalities, check you own policy for coverages)

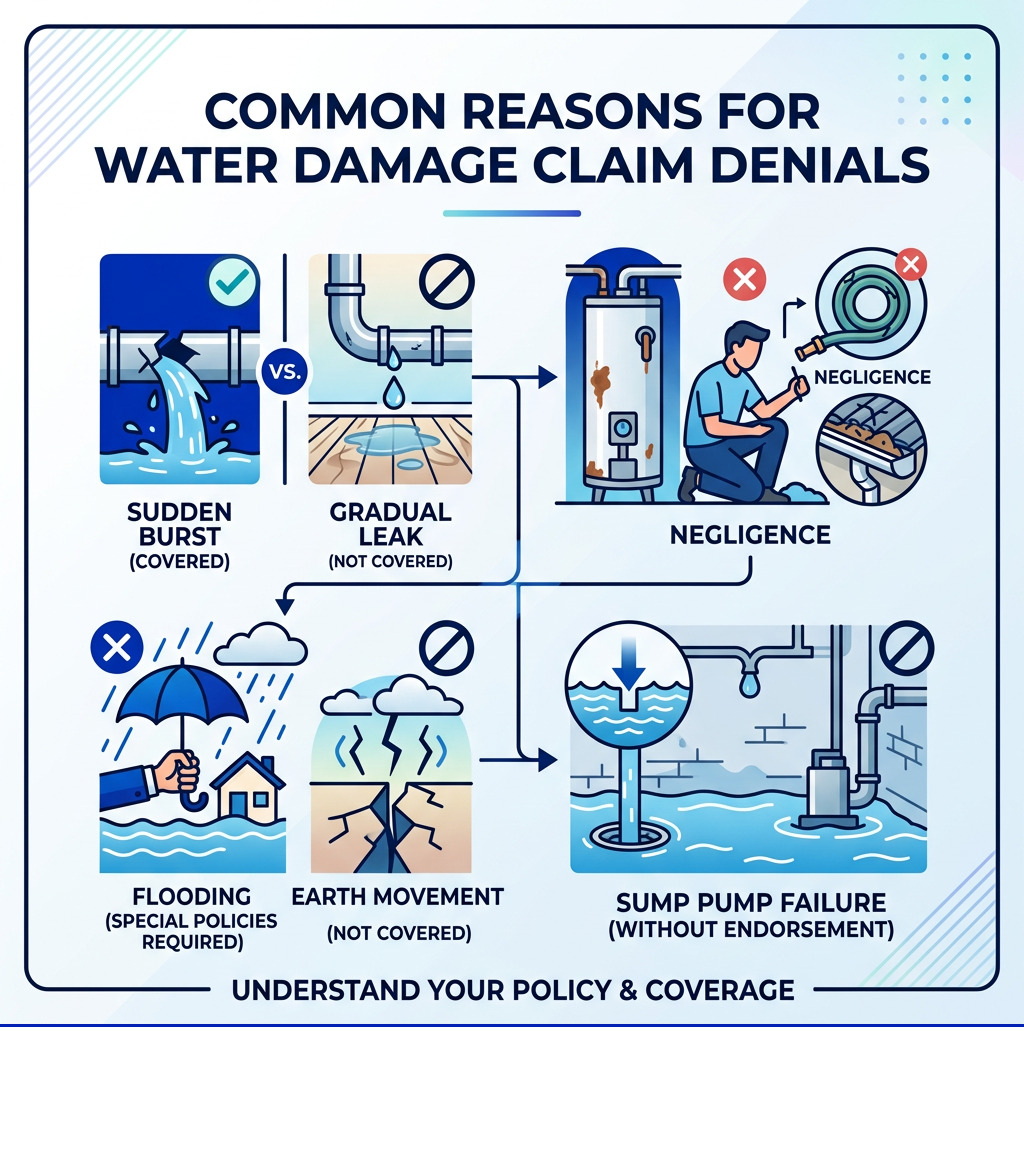

- Gradual damage – slow leaks or seepage over time are treated as maintenance issues, not covered events

- Lack of maintenance – corroded pipes, aging roofs, or neglected appliances can void your claim

- Flood exclusions – standard homeowners policies do not cover flooding; that requires separate insurance

- Sewer backup or sump pump failure – excluded unless you added a specific endorsement

- Poor or incomplete documentation – missing photos, receipts, or moisture reports weakens your case

- Late reporting – waiting too long to file can give the insurer grounds to deny

- Failure to mitigate – not taking steps to stop further damage after discovery

- Policy exclusions for mold, seepage, or groundwater – often excluded even when connected to a water event

Water damage is far more common than most homeowners expect. Around one in 60 insured homes files a water or freezing claim each year. The average claim costs over $10,000 — and in serious cases, repairs can run well past $100,000.

So when your insurer denies or underpays that claim, the financial impact is real and immediate.

The hard truth is that not all water damage is treated the same way by insurance companies. A burst pipe that floods your kitchen in minutes is handled very differently from a slow drip behind your wall that went unnoticed for months. Understanding that difference — and knowing how to document and report what happened — can make or break your claim.

This guide walks you through exactly why claims get denied, what your policy likely covers (and doesn’t), and what you can do if you’re already facing a denial. Whether you’re in the middle of a claim or just trying to prepare, we’ll help you understand what’s happening and what your real options are.

At Hudson Douglas Public Adjusters, we work exclusively for property owners — not insurance companies. We’ve seen these denials up close, and we know how to navigate them.

Similar topics to why insurance not paying my water damage claim:

Common Reasons Why Insurance is Not Paying My Water Damage Claim

When you discover standing water in your living room or a soft spot in your drywall, your first call is often to your insurance company. You expect them to have your back. However, many residents in Scottsdale, Mesa, and Gilbert find themselves staring at a denial letter.

The most frequent reason we see for a denial is the distinction between “sudden and accidental” damage and “gradual” or ” long term” damage.

Sudden vs. Accidental Damage

Standard homeowners policies are designed to cover events that happen in an instant—unexpected, unintended, and immediate. Think of a washing machine hose that snaps while you’re at work, or burst pipes that flood a basement overnight. These are typically covered because you couldn’t have prevented them through routine upkeep.

The Problem of Gradual Damage

On the flip side, if the water damage is deemed “gradual,” the insurer will likely point to a lack of maintenance. This is a primary reason why insurance not paying my water damage claim becomes a reality for many. If a pipe has been pinhole-leaking for six months, causing rot and mold, the insurance company views this as a failure of the homeowner to maintain the property. They argue that if you had inspected your plumbing or noticed the rising water bill, the damage could have been avoided.

Maintenance Neglect and Wear and Tear

Nearly a quarter of all homeowners’ insurance claims in a recent year involved water damage, and a significant portion of those denials stem from “wear and tear.” Insurance is not a home maintenance plan. If your roof is 30 years old and starts leaking because the shingles are crumbling, that isn’t a “loss”—it’s an expired product.

For more context on these nuances, read our guide on Why Covered Water Damage Isn’t Always Covered. We often find that insurers use the “maintenance” excuse as a blanket denial, even when the damage was truly hidden and impossible to see. For More info about water damage claims, you can explore how we categorize these losses to fight for a fair payout.

Understanding Policy Exclusions: Floods, Sewers, and Seepage

One of the biggest shocks for property owners is realizing that “water damage” and “flood damage” are two entirely different things in the eyes of an insurance company.

The Flood Insurance Gap

Standard homeowners insurance almost never covers flood damage resulting from water rising outside the home. Whether it’s a flash flood in Phoenix or heavy rains in St. George, if the water touched the ground before entering your home, it’s likely classified as a flood. To be covered, you need a separate policy through the National Flood Insurance Program (NFIP) or a private flood carrier. You can Check if you live in a FEMA-designated flood zone to see your risk level.

Sewer Backups and Sump Pump Failures

Another common exclusion involves “water backup and sump overflow.” If a city sewer line backs up into your home or your sump pump fails during a storm, your standard policy will likely deny the claim unless you have a specific endorsement (a “rider”) for this. This is a common pitfall we see in areas with older infrastructure or heavy seasonal monsoons. Understanding the difference between Flood Damage vs Water Damage Arizona is critical for setting your expectations correctly.

Groundwater Seepage and Foundation Cracks

If water seeps through your foundation or basement walls because of a high water table or poor drainage, insurance typically calls this “groundwater seepage.” Because this is often a result of the home’s construction or the surrounding soil conditions, it is almost always excluded.

However, some “floods” aren’t natural. For example, a Fire Sprinkler Flood in a commercial building or high-rise is usually covered under the building’s property policy because it originates from an internal system, not the rising tide.

How Documentation and Timing Affect Your Payout

Documentation is the “evidence” in your case. Without it, the insurance company gets to tell the story—and their story usually ends with them paying less.

Timely Reporting is Mandatory

Most policies require you to report a loss “immediately” or within a very specific timeframe (sometimes as short as 60 days). If you wait to file a claim because you’re trying to dry it out yourself, the insurer may deny the claim because your delay allowed mold to grow or the damage to worsen.

Your Duty to Mitigate

You have a contractual obligation under your policy to “mitigate” the damage. This means you must take reasonable steps to stop the water from causing more harm.

- Shut off the main water valve.

- Move furniture out of standing water.

- Call a professional to start the drying process.

If you don’t take these steps, the insurer might only pay for the initial burst and deny the subsequent rot or mold.

Evidence Collection and Moisture Mapping

Before you start throwing away soaked carpet or cutting out drywall, take photos and videos of everything. Insurance adjusters need to see the “origin” of the leak. If you fix the pipe and throw away the evidence before they arrive, they may deny the claim because they can’t verify the cause.

We recommend following our Water Damage Insurance Claim Tips to ensure you don’t miss a step. One of the most important tools we use is moisture mapping—using infrared cameras and moisture meters to prove that water traveled further than the naked eye can see. To learn more about the filing process, check out Don’t Get Damaged Twice.

What to Do if Your Water Damage Claim is Denied

If you’ve received a denial, don’t panic. It is not the final word. In our 40+ years of experience, we have seen many “final” denials overturned with the right approach.

1. Review the Denial Letter Carefully

The insurance company is legally required to tell you exactly which part of your policy they are using to deny the claim. They will quote specific language—look for words like “gradual,” “seepage,” or “maintenance.”

2. Get Independent Estimates

The insurance company’s adjuster works for the insurance company. Their estimate is often based on the lowest possible cost. A Public Adjuster can provide you with an independent evaluation of your loss, at times help from a licensed contractor is utilized. Contractors are not licensed to adjust your claim. This provides a counter-argument to the insurer’s lowball offer.

3. The Appeal Process and Claim Supplements

If the insurer missed the full scope of the damage (which happens often), you can file a “claim supplement.” This is additional documentation showing that the repairs will cost more than they initially estimated. For a step-by-step guide, see our Denied Water Damage Claim Guide.

4. Watch for Signs your carrier is not acting in Good Faith

In Arizona and Nevada, insurance companies have a “duty of good faith and fair dealing.” If they are ignoring your calls, refusing to investigate, or denying a claim without a reasonable explanation, they may not be acting in good faith. You can learn more about this in our article on Signs Insurance Company Underpaid.

We specialize in taking you From Leak to Loot, ensuring that every square inch of damage is accounted for and paid for.

Frequently Asked Questions About Why Insurance is Not Paying My Water Damage Claim

| Feature | Sudden & Accidental | Gradual Damage |

|---|---|---|

| Example | Burst pipe, appliance failure | Slow leak behind wall, seepage |

| Discovery | Immediate | Weeks or months later |

| Coverage | Typically Covered | Typically Excluded |

| Cause | Unexpected event | Lack of maintenance/Wear & tear |

Why is my insurance not paying my water damage claim for a slow leak?

Insurance companies classify slow leaks as “gradual damage.” Their logic is that a homeowner should have noticed the leak through regular inspections or a spike in the water bill. However, if the leak was hidden inside a wall or under a slab where it couldn’t be seen, we can often argue that the “discovery” was sudden, even if the leak was gradual. If you’re dealing with a Burst Pipe Insurance Claim that the insurer is calling “old,” we can help prove otherwise.

Can I appeal if insurance is not paying my water damage claim?

Yes, you absolutely have appeal rights. You can submit new evidence, such as a report from a leak detection specialist or a structural engineer, to challenge their findings. If you feel you aren’t being heard, a Denied Water Damage Claim can be reopened and re-evaluated with the help of a Public Adjuster.

Does homeowners insurance cover mold after a water claim?

Mold is a tricky subject, check your policy language. Most policies have a “mold limit” or “remediation cap,” often between $5,000 and $10,000. If the mold is a “resulting loss” from a covered water event (like a burst pipe), it is usually covered up to that limit. However, if the mold grew because of high humidity or a slow, unaddressed leak, it will likely be denied. This is common with Dishwasher Leak Damage, where water can sit under the unit for weeks before mold is discovered.

Get a Local Expert on Your Side

Dealing with water damage is stressful enough without having to fight your insurance company. If you’re wondering why insurance not paying my water damage claim, the answer usually lies in the fine print of your policy and the way the damage was documented.

At Hudson Douglas Public Adjusters, we are a family-owned and operated business with over 40 years of experience. We are locally based in Arizona, serving communities from Scottsdale and Paradise Valley to Mesa, Goodyear, and beyond. We also proudly serve clients in Clark County, Nevada, and the Utah Wasatch Front.

We work solely for you, the policyholder. We don’t get paid unless you do—our fee is a small percentage of the payout, and there are never any out-of-pocket costs for our services. Whether you need help in English or Spanish (Hablamos Español), our team is available 24/7 to ensure you get the settlement you deserve.

Don’t let a denial leave you underwater. Contact a professional public adjuster for a free claim review today, and let us handle the insurance company while you focus on getting your home back to normal.